By Joseph Webster and William Tobin

Chinese influence in Latin American energy is large and impactful, ambiguous, and potentially risky in certain contexts. Russian influence, on the other hand, is limited, sharply receding, and seems to have few purposes beyond opposing US interests. Western policymakers should seek to prevent Beijing from cementing a long-term monopoly in regional energy supply chains; offer credible investment and partnership alternatives, especially in strategic sectors, including critical minerals; and excise Moscow’s malign influence to the greatest degree possible. Finally, US policymakers should also look to reach some oil market détente with Venezuela, despite the Maduro regime’s brutality, as Venezuelan crude exports pressure Russian energy earnings. Moreover, given Moscow’s and Beijing’s different and potentially incompatible interests in Venezuelan oil, Washington and Brussels could leverage this issue to drive a slight wedge between them.

Chinese influence in Latin American energy

Oil: Brazil and Venezuela

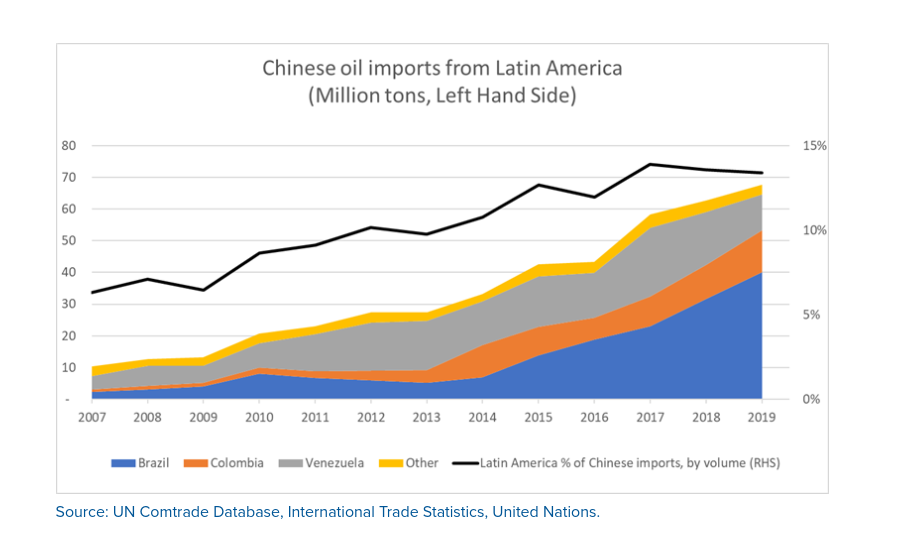

China’s involvement in Latin American oil markets has expanded dramatically since 2005 but may be plateauing. From 2005 to 2017, the region received about $30 billion in foreign direct investment in the oil and gas sector, routed primarily to Brazil, Argentina, Venezuela, and Peru. China also lent about $98 billion to the Latin American oil and gas sector from 2007 to 2016. Chinese volumes of crude imports from Latin America grew 556 percent from 2007 to 2019, as shipments from the region accounted for nearly 13 percent of all Chinese crude oil import volumes. Latin American crude oil exports after 2019 are more difficult to calculate due to the opacity of Venezuelan data.

China’s growing involvement in Latin American energy came at an opportune time for the region’s oil and gas producers. The great financial crisis and resulting demand shock damaged the region’s balance sheets, while the US tight oil boom dented Latin America’s crude export prospects. China’s outward investment and massive, energy-intensive stimulus package in 2009 established itself as an alternative market for Latin American producers, although its regional oil market influence became more complicated in 2018 due to stricter US sanctions on state oil company Petróleos de Venezuela SA (PDVSA) and the election of Jair Bolsonaro in Brazil.

Chinese energy influence is pronounced in Brazil, the region’s largest crude oil exporter. Crude oil exports to China accounted for nearly 47 percent of all Brazil’s 2021 crude exports, as measured by value, and nearly 0.9 percent of Brazil’s gross domestic product in the same year. Brazil and China have become increasingly intertwined in oil markets. In 2009, China International United Petroleum & Chemicals (Unipec) and Brazilian national oil company Petróleo Brasileiro, aka Petrobras, reached a supply agreement guaranteeing 200,000 barrels per day from 2010-2019 and a $10 billion loan from the China Development Bank. In Brazil, China Petrochemical Corporation (Sinopec), the parent of Unipec, formed a partnership with Petrobras, beginning in 2010, to gain expertise in offshore drilling. From 2007 to 2020, China invested roughly $66 billion into Brazil, with the oil and gas sector comprising nearly 30 percent of its investment.

All indications suggest China has become Venezuela’s most important customer, although transparent data is lacking. Following the tightening of sanctions in August 2019 by the Trump administration, China’s flagship national oil and gas company, Chinese National Petroleum Corporation (CNPC), stopped transporting crude from Venezuela to route to Chinese demand centers. Facing sanctions, Beijing’s “dark fleets” played a large role in transferring Venezuelan oil to China. Much trade from Venezuela to China is masked under third countries. For instance, from May 2020 to June 2021, the volume of “Malaysian bitumen” shipments which were routed to China rose thirteenfold; however, Vortexa Analytics estimated that about 90 percent of April 2020–April 2021 cargoes were in fact Venezuelan crude, according to a Reuters article. A prominent analyst of Venezuela’s oil sector, Dr. Francisco Monaldi, conveyed his estimate via email to the authors that approximately 85 percent to 90 percent of Venezuela’s oil output is routed to China, a share which has slightly decreased as more exports have been routed to the United States.

Venezuelan oil exports have been routed through clandestine tanker-owning organizations within the Chinese defense establishment. The Biden administration’s push to relieve sanctions on Venezuela’s oil sector, exemplified by the November 26, 2022, decision to renew Chevron’s license to produce and export oil from Venezuela through “License 41” is seen by many analysts as an attempt to bring greater transparency to the market. Through this “legitimizing” of Venezuelan oil production, more exports can theoretically be routed through trackable registered tankers.

The new license for Chevron to export oil from Venezuela has decreased China’s share of Venezuela’s exports slightly and contributed to an increase in Venezuela’s aggregate oil and oil products production to roughly 750,000 barrels per day, from about 680,000 barrels per day in October 2022, per secondary sources.

Critical minerals: Chile, Argentina, Peru, and Bolivia

China has long sought to secure the critical industrial and technological metals value chain as part of its economic strategy. Critical minerals such as copper and lithium are vital for energy technologies like electric vehicles (EVs), solar panels, wind turbines, etc. And China consumes roughly half of the world’s annual output of industrial metals, such as copper, steel, and aluminum. Due to Beijing’s desire to dominate strategic industries, as well as Latin America’s abundant natural resources, China invested $16 billion in the region’s mining sector between 2018 and 2020.

The Latin American region, particularly the countries of Chile, Peru, and others across the Andean Ridge, are endowed with monumental reserves of copper, totaling at least 313 million tons, or about 35 percent of global reserves. Latin America has therefore seen considerable interest from Chinese investors and traders.

Chilean state copper producer Codelco and private companies like SQM have developed robust relationships with Chinese metal traders such as Xi’an Maike Metal International Group, while international trading houses like Glencore have made strategic bets on Chinese commodity demand (or acquired firms like Xstrata, which had done so). These firms route copper to Chinese smelters and warehouses, feeding sectors like construction and, increasingly, the energy sector. China has also begun to invest directly in major copper mining operations abroad, like the Las Bambas mine in Peru, which is now wholly owned by a Chinese consortium and produces 2 percent of the global copper supply on its own. This consortium, led by the Minerals and Metals Group (MMG Limited), plans to provide $2 billion to expand the mine’s production and meet copper demands from the energy transition. Peru’s political unrest in early 2023 substantially curtailed production from this operation in 2023, however, and has cast doubts on the future of investment in the country’s mining sector.

In addition, lithium is increasingly prominent due to the growing demand for lithium-ion batteries, and Latin America boasts considerable reserves of the strategic metal. Chile and Argentina are the world’s second- and fourth-largest producers of lithium, which has been the focus of considerable Chinese regional investment.

Chinese corporations Tianqi Lithium and Ganfeng Lithium, the world’s second- and third-largest lithium miners, respectively, are major regional players. Ganfeng Lithium is a major joint-venture partner in the development of Argentina’s flagship lithium projects, Cauchurí-Olaroz and Mariana. Tianqi Lithium, meanwhile, obtained a 23.77 percent share in Chile’s flagship private lithium producer SQM in 2018. Together with Zijin mining’s $380 million investment in the Tres Quebradas lithium project, among other projects, Chinese miners have become formidable actors in Latin America’s strategic metals.

Electricity markets and renewables: Brazil, Chile, and Peru

China’s influence in Latin American electricity markets is significant and, in some cases, dominant. China is an influential investor across the region’s generation, transmission, and distribution segments; enjoys a virtual monopoly in solar panels in the region (as it does globally); is a major (but not dominant) player in Latin America’s onshore and offshore wind markets; and is seeking to gain a foothold in Argentina’s nuclear power plant industry.

According to a recent working paper by Pedro Henrique Batista Barbosa, Chinese companies owned about 10 percent, 12 percent, and 12 percent of Brazil’s generation, transmission, and distribution segments, respectively; placing China as the second, third and fourth most significant foreign investor in these sectors. Elsewhere in Latin America, China’s Yangtze Power International purchased assets of Sempra Energy, a US-based utility, while China’s State Grid acquired Sempra’s Chilean assets.

China’s dominant role in regional and global solar supply chains could enable it to exert political influence and should elicit some response from Western policymakers. The International Energy Agency (IEA) reports that nearly 97 percent of solar wafers originate in China. Accounting for over 98 percent of Brazil’s imports of solar panels in 2021, China also exerts an astonishing dominance in the region’s solar markets. Moreover, with regional solar generation capacity set to rise exponentially due to outstanding sunlight resources, climate targets, and declining hydropower generation, China’s dominance of solar supply chains could be translated into political leverage in the future.

An IEA study finds that China’s annual output of solar photovoltaic capacity could exceed its domestic deployment needs by over 750 gigawatts (GW) in 2030. To put those figures in context, the world’s total cumulative solar deployment capacity stood at 1,053 GW in 2022. Consequently, China is on pace to flood the world market—and Latin America—with solar panels if it can continue its industrial subsidies.

China’s growing solar exports present considerable opportunities and risks for Latin America. On the one hand, cheap solar panels could reduce the region’s emissions while lowering electricity costs and improving grid resiliency, especially on hot days. Conversely, however, imports of Chinese finished products could leave Latin America with few chances to capture value along the solar supply chain. The risks are especially great if Chinese companies own a monopoly of the electricity sector, from generation to transmission to retail. Some security experts have also raised the possibility that Chinese-made solar inverters could be installed with components that enable backdoor hacking, although other experts believe the energy sector has bigger vulnerabilities.

There are already indications that Chinese companies are seeking to capture the solar value chain in Latin America by purchasing local power suppliers. One concerning example is in Peru. China’s state-owned Southern Power Grid International is seeking to purchase the electricity assets of Enel, which currently generates and supplies electricity for over half the population of Lima, Peru’s capital city. Should Chinese companies capture the entirety of the solar value chain, Latin America will be shut out of the profits of a green transition. Even more worrisome, however, is the possibility that Beijing would use its monopoly of electricity markets to extract geopolitical concessions from the region. Latin America and its friends should take a balanced approach to China’s role in regional solar markets. While cheap solar panel imports could prove highly beneficial for the region’s developmental needs, regional capitals, along with Washington and Brussels, should ensure that Latin America retains key aspects of the supply chain. As is the case with other technologies, regional capitals must determine how much risk is tolerable and which critical infrastructure must be protected.

Latin America is at much less risk of falling prey to a sole supplier in onshore and offshore wind markets, which will play an increasingly important role in the region’s energy mix due to declining hydropower generation and climate objectives. Brazil is a wind manufacturing and export hub already, and installed 80 percent of all incremental wind power capacity in Latin America in 2022. While China has installed more onshore and offshore wind capacity than any other market, it does not dominate world or Latin American export markets.

China’s role in regional wind markets will be worth watching, however. General Electric stopped producing turbines in Brazil in 2022, while China’s Goldwind is expected to establish a new wind turbine facility and start deliveries in 2024. Still, European developers may be well positioned to best Chinese competitors, as Shell and Equinor have a head start in Brazil’s offshore wind markets.

China is on pace to embed itself in future Latin American green hydrogen supply chains, due to its dominance of solar and electrolyzer production. China could also eventually import green hydrogen from Latin America via an ammonia or methanol carrier, although maritime hydrogen transportation may not be viable for a decade or longer, if at all.

Entry into the region’s nuclear power markets have proved difficult for Chinese companies. In February, China and Argentina inked an agreement over an $8 billion nuclear power plant, with Beijing agreeing to finance 85 percent of the cost. That deal has been put on ice, however, due to Buenos Aires’s demands about manufacturing the reactor fuel domestically. Beijing may be willing to provide considerable concessions to Argentina due to industrial policy motivations: China hasn’t sold a single reactor outside of Pakistan, while Romania canceled a deal with Beijing in 2020 in favor of working with the United States.

Russian influence in Latin American energy

Russia is a relatively minor—but not inconsequential—player in Latin America and seeks to use its regional energy influence to bolster pro-Kremlin figures and oppose US interests. Russia exercises substantial influence in Venezuelan and Cuban oil markets; while its exports of natural gas-produced fertilizers are important for the region’s agriculture, they are beyond the scope of this paper.

Roszarubezhneft, a Kremlin-owned oil company, has produced as much as 15 percent to 20 percent of Venezuela’s total oil output. Independent sources believe Russia has extended at least $17 billion in loans and credit lines to Venezuela since 2006, with Russian oil company Rosneft providing a $6.5 billion loan to PDVSA, Venezuela’s state oil company. Still, ties are complicated as Russia and Venezuela supply similar crude grades and compete for customers. PDVSA recently seized control of a minority stake in a joint venture run by former Gazprom officials. Pulling on this thread and seeking to increase Venezuelan crude output and exports may prove fruitful for Western policymakers, as Moscow has little to offer Caracas. Moreover, additional Venezuelan barrels would provide more supply certainty to Washington and Brussels amid tensions with Russia and Iran, two major oil suppliers.

Russia is also shipping crude oil to Cuba, which relies on fuel oil imports for its electricity needs. With the island’s communist regime facing persistent electricity blackouts, economic protests, US sanctions, and natural disasters, Havana enjoys substantial economic and political benefits from Russia’s crude oil imports. Some experts believe Russia is either extending Cuba extra credit or that Venezuela is indirectly funding Russian oil exports to Cuba via promises of future oil payments. Through careful, sure-footed diplomacy, Washington may be able to use the situation to its advantage and excise Russian influence from Cuba. Easing US crude oil export sanctions on Havana could displace Russian exports; secure important concessions from Havana, especially on humanitarian issues; and support US exports and jobs.

Finally, Russian energy influence was an element in Brazil’s 2022 presidential elections. Former Brazilian President Bolsonaro visited the Kremlin on February 16, little more than a week before Moscow’s invasion of Ukraine, to say Brazil was in “solidarity” with Russia. Over the summer, in the run-up to Brazil’s October 2022 presidential election, Bolsonaro sought Moscow’s support in obtaining diesel and fertilizer shipments, which would have benefited his candidacy in key constituencies, such as the trucking industry. Bolsonaro also criticized his own vice president, Hamilton Mourao, for speaking out against the invasion. Bolsonaro’s government engaged in significant price cutting of refined products ahead of the elections, as Brazil reportedly received two tankers of Russian diesel in the fall. While the degree of Putin’s intervention in Brazilian internal politics is uncertain, there is substantial evidence that Bolsonaro sought to leverage Russian energy for his own personal domestic political interests.

Recommendations

US policymakers should:

- Help to ensure that Latin America can credibly look beyond Beijing for energy partners, working with like-minded partners, especially in renewable energy supply chains. China’s near monopoly along segments of the region’s solar supply chain, for instance, is a major risk for Latin America, given that solar power will be an important driver of the energy transition. The United States must continue to bolster its own clean energy manufacturing capacity and develop its own exports of clean energy technologies and services to provide an alternative for Latin American markets. Whenever possible, it should encourage and finance renewable industrial development across the value chain in Latin America.

- Raise awareness of the risks of sole-supplier dependency in key markets, especially in the utilities sector, but also provide viable and credible alternatives. While imports of Chinese solar panels provide both opportunities and risks for the region, allowing Chinese companies to capture the entirety of the solar value chain will limit Latin America’s benefits while potentially exposing the region to uncompetitive markets and geopolitical risks, even geopolitically motivated electricity shutoffs. When appropriate, the West should provide support for firms seeking to make investments in energy infrastructure in Latin American nations, particularly as an alternative to Chinese firms seeking to establish monopolies.

- Work to excise Moscow’s malign regional influence in Venezuela and Cuba. While Beijing’s regional influence presents both threats and opportunities for both Latin America and the United States, the Kremlin’s regional energy policy is largely aimed at undermining US interests. The United States should seek to return Venezuelan crude to the market and reduce Moscow’s export earnings, as Venezuela’s Merey crude grade competes with Russia’s Urals blend. Moreover, risks with Iran pose an underrated threat to energy supply security, necessitating additional barrels on the market. The national security stakes are lower in Cuba, but there may be opportunity to reduce Russian exports and secure humanitarian concessions from Havana in exchange for easing US oil export restrictions. Through skillful diplomacy and the judicious application of carrots and sticks, Washington may be able to sharply reduce Russian influence in Caracas and Havana and inject a moderate irritant into Beijing-Moscow ties, as the two governments have differing regional interests and strategies.

- Continue to grapple with the real interests and needs of Latin America, as well as the limitations of US power. Tens of millions of individuals in Latin America suffer from insufficient access to energy and electricity, which has been exacerbated by Beijing’s mishandling of COVID-19 and Putin’s invasion of Ukraine. While the region may be willing to curtail Moscow’s influence, given Russia’s limited economic footprint, economic partnership with China is a fact of life for Latin America. US policymakers should therefore continue to develop frameworks to stimulate investment in Latin America in areas such as “nearshoring” for manufacturing, support financing alternatives that compete with Chinese energy investment, and continue to work with regional and out-of-region allies and like-minded partners. These steps will not only benefit the region but also US interests more broadly.

This Blog has been sourced from Atlantic Council and can be accessed here