This is an extract from a recent paper “Actualizing the green hydrogen economy” prepared by Deloitte. This paper reviews the green hydrogen landscape providing insights on current and developing law and policy frameworks, finance, and bankability considerations, and provides recommendations to help advance the green hydrogen value chain considering key challenges and areas of opportunity.

Economic and financial characteristics of green hydrogen

Green hydrogen can be produced via electrolysis of water using wind and solar electricity, therefore virtually everywhere. However, the cost of green hydrogen production can vary significantly across different geographies with a key element influencing the cost of green hydrogen, being the production yields of the renewable power plants, stemming from solar irradiation and wind speed. As the plant yield of a renewable power source increases, the higher the plant production for a given installed capacity, which then drives down the cost of the electricity production. This, in turn, reduces the cost of the green hydrogen production. The average cost of hydrogen production can be defined using the Levelized Cost of Hydrogen (LCOH) metric. LCOH accounts for all capital and operating production costs in the levelized manner over a unit of produced hydrogen and its derivative (US$/kg).

In 2050, producing solar PV-based green hydrogen in North Africa could cost one-quarter of European production. Benefiting from high renewable (especially solar) endowments, green hydrogen produced in Australia, Chile, Mexico, northern and sub-Saharan Africa, and Middle Eastern countries can be highly cost competitive. Moreover, the widespread availability of land in these regions for renewable installations, compared to those with limited land availability (such as Japan, Korea, and some parts of Europe) makes these regions more adapted for development and exports of green hydrogen.

The cost competitiveness of green hydrogen does not only depend on wind and solar potentials. Green hydrogen is a highly capital-intensive technology that requires significant investments. Production costs of green hydrogen consists of investments in renewable power plants, electrolyzers, their connection equipment, the fixed operation and maintenance costs and the cost of water consumed for its production. Therefore, the bulk of the LCOH consists of investment costs, and its cost elements are largely fixed costs.

A key challenge regarding the development of green hydrogen is the availability of liquidity. Many of the regions that have significantly high green hydrogen supply potential suffer from lower availability of financing options for the required investments. Therefore, access to investment funds in such regions can be identified as one of the critical measures needed to help solve the bottlenecks regarding the development of a global costcompetitive green hydrogen value chain.

Highly capital intensive in nature, green hydrogen projects require raising significant amounts of debt and equity, which can adversely impact financing costs and competitiveness of investments. An important factor influencing financing costs is the country’s political risk level. Some of the most promising locations for green hydrogen projects may suffer from high country-related political risks. In practice, private investors and lenders expect higher rates of return to compensate for greater political risks.

Such perceived risks are translated into a higher weighted average cost of capital (WACC) for the projects, which acts as an interest rate therefore, increasing the overall cost of the project via additional financing costs. Access to affordable finance can be a critical enabler for green hydrogen projects.

Project development timelines can be a major bottleneck in scaling up the production of green hydrogen that consist of two major processes: permitting procedures and construction. Permitting schemes for renewable energy projects can bring significant delays to the operation of the power plants. After an investment decision, once the expenditure allocations are done, the permitting and validation procedures as well as the construction operations can bring not only delays, but also resulting financial losses due to the blocked liquidity and applied interest during the operation. Minimising the delays and the financial costs of the projects will require accelerated and streamlined permitting processes and construction.

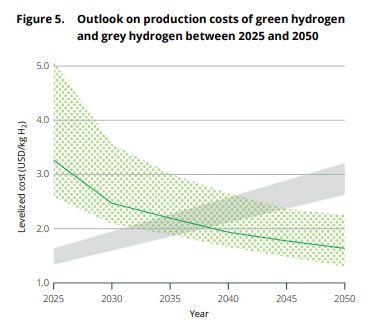

Like renewables, which have experienced significant cost reduction over the last decades, the manufacturing cost of green hydrogen equipment is projected to fall steeply in the coming decades. Green hydrogen is expected to become one of the most cost-competitive hydrogen production technologies in the long run. In 2050, levelized production costs could fall below $1/kgH2 in Chile, and below US$1.1/kgH2 in north and sub-Saharan Africa, Mexico, China, Australia, and Indonesia. Yet, currently green hydrogen is the most expensive one, and it is expected to remain generally more expensive than the carbon-intensive gray hydrogen at least until 2035. Therefore, to help create a level playing field, green hydrogen projects need support through operational premiums until they are commercially competitive.

Development of a global green hydrogen value chain has a twofold challenge: decarbonization of its current uses, and creation of new hydrogen uses. Currently, industry consumes about 95 million tons of hydrogen globally, nearly entirely produced from fossil sources. In a climate neutral world, clean hydrogen can become the second biggest final consumed energy carrier. While some of these end-uses can consume hydrogen by simply replacing the initial commodity by it, in most of the cases a significant infrastructure and equipment shift is needed. For instance, hydrogen for the road transport sector requires a complete change of the vehicle engines, from internal combustion engines to electric motors, including fuel cells.

Economic and financial support to help produce green hydrogen should be complemented with the creation of demand signals for clean hydrogen and its derivative molecules in different sectors. Initiation of a clean hydrogen economy, in line with the Sustainable Development Goals, requires

1. Facilitating investments via unlocking funds and foreign investment initiatives,

2. Reducing financing costs via enabling access to low-cost finance

3. Creating a level-playing field for green hydrogen via operational subsidies until at least late 2030s

4. Creation of demand for green hydrogen via sectoral initiatives and obligations

5. Reduction of the permitting and construction periods via facilitated permitting processes.

Overview of some of the main financial and economic instruments to help increase bankability of green hydrogen projects

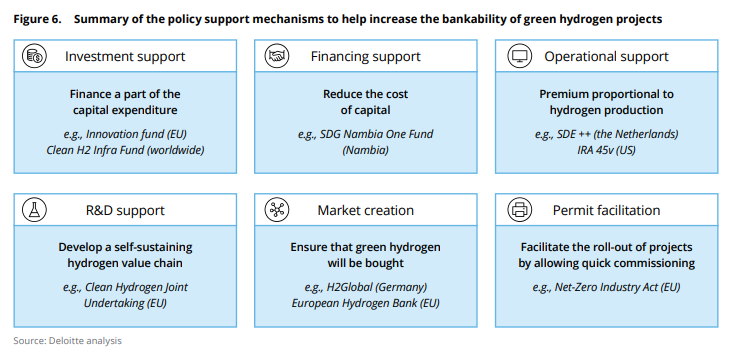

Several mechanisms can be used to help make green hydrogen projects economically more competitive and to facilitate investments. Potential policy support schemes can be grouped as follows: investment support, financing support, operational support, R&D support, market creation and permitting facilitation. Figure shows these support mechanisms.

Investment support mechanisms can reduce the amount of money required to build production capacities. There are many funds that support green hydrogen projects by financing a part of their capital expenditure (CAPEX). In Europe, the Innovation Fund supports up to 60% of a project’s CAPEX and a variable fraction of its operational expenditures (OPEX) incurred in the first 10 years of operation. The Connecting Europe Facility for Energy (CEF – E) is an EU funding instrument for targeted infrastructure investment at European level. Such funds inject liquidity into projects and help reduce the required investments.

IEA states that 65% of the funding required to reach net-zero emissions must come from the private sector. However, in developing countries where renewable hydrogen production is more promising, private investors and lenders expect higher rates of return to compensate for greater political and operational risks resulting in higher WACC levels. Financial support mechanisms, such as guarantees can help to reduce country risk premium and thus the cost of capital, making the projects more bankable. The European Investment Bank (EIB) offers solutions in the form of guaranteed instruments in markets where there is a lack of investment. EIB also at times guarantees potential losses from a project. Blended finance mechanism is another financial support mechanism that can mobilize private investments alongside sustainable development outcomes to help increase the bankability of the projects. Currently, green hydrogen projects suffer from a lack of financial support mechanisms, entailing lower bankability for such projects.

Operational subsidies are often designed as a premium that varies with hydrogen production functioning as a subsidy to compensate for the difference between the production cost (LCOH) and the revenues.

In Europe, the Clean Hydrogen Joint Undertaking supports research and innovation in hydrogen technologies, with the scope including renewable hydrogen production, distribution, storage, and use for transport and energy-intensive industries. Targeting establishment of new knowledge, exploration of the feasibility of a new technology, support actions for standardisation and the development of prototypes, demonstrations, or pilots, the CH-JU provides economic support mainly through grants and is endowed with about $1 billion funding completed with more than $1 billion from private sources. The CAPEX of projects that are expected to have a significant impact in accelerating the transition to a hydrogen economy may also be considered as an eligible cost.

Another reason for underinvestment is the lack of a proper market for green hydrogen. It is necessary to develop the potential market and to use offtake agreements or compensation mechanisms to help ensure that the hydrogen produced will be bought. As with contracts for difference (CfD), the difference between suppliers’ lowest bids and buyers’ highest bids is compensated by grants from a public or philanthropic funding body. The revenues are secured for the producers, which is attractive for investment, and importers gain access to green derivatives. At the European level, the Commission is designing the first pilot auctions on renewable hydrogen production, named the ‘European Hydrogen Bank’ (EHB).

Carbon quotas, carbon taxes and green certificates/guarantees of origin can increase the demand for green hydrogen, facilitating the creation of its market. The EU Emissions Trading System both raises money for the Innovation Fund and helps create demand for clean hydrogen. Some countries like France or South Africa already have carbon pricing schemes in place. These schemes help increase the cost of carbon-intensive grey hydrogen and thus make green hydrogen more competitive.

A few institutions already deliver green hydrogen certifications, such as CertifHy in the EU, TÜV SÜD in Germany, the Aichi Prefecture in Japan, or the China Hydrogen Alliance. In the same way, the EU taxonomy creates a frame of reference for investors and companies. Certification works to signal credible green projects for investors to invest in. Even if it is not linked to any financial benefits, the taxonomy works as an incentive to help scale up investment in green projects.

Finally, non-monetary support mechanisms to help accelerate permitting processes and reduce construction delays can be an important facilitator to roll-out of green hydrogen projects. Reducing permitting times and ensuring the timely availability of materials can attract investments by reducing project risks.

Effectiveness of the main financial and economic instruments

A case study is utilised to help illustrate how various support mechanisms presented in the previous section impact the economic and financial viability of green hydrogen projects. Analysis considers the cost and financial indicators of a green hydrogen production project via electrolysis using solar power in Southern Africa.

- Financing support

Today, with current financing conditions, the WACC in countries in Southern Africa is higher than that of European countries. This is, at least partially, due to its higher country risk that stems from political, institutional, and regulatory risks. Compared to a European country, the investments bring much higher financial costs. Deloitte chose Southern Europe (as the region with the highest solar potential, and therefore, lowest LCOH in Europe) as a comparison reference.

In current financial conditions, the cost of green hydrogen produced in Southern Africa is slightly higher than the cost of the one produced in Southern Europe, although Southern Africa holds better renewable potential than Southern Europe. Each year, more hydrogen can be produced with fewer electrolyzer and solar panel capacities in Southern Africa. Even if financing costs are higher in Southern Africa due to its higher WACC, investment costs are lower. While financing costs represent 35% of the LCOH in Southern Europe, it accounts for more than 50% of it in Southern Africa. The solar-based green hydrogen in Southern Africa with a WACC of 6% costs 25% less than the same in Southern Europe.

- Operational and investment support

Considering the same case study (solar-based green hydrogen production in Southern Africa), Deloitte analyses the effect of an operational premium-type support, similar to the US Inflation Reduction Act. With a premium of US$3/kgH2 for 10 years, the green hydrogen LCOH is decreased by 45%. This accounts for an overall support of US$1.3 million for the considered project over 10 years. The same premium of US$3/ kgH2 over 20 years brings the LCOH down to US$1.36/kgH2, in turn making green hydrogen cost competitive with grey hydrogen. However, it should be noted that such a subsidy does not necessarily amount to twice the same subsidy over 10 years. This is due to the discount rate, which also adds the annual interest rates to the equation.

To help assess the effectiveness of operational premiums and investment support mechanisms comparatively, this analysis assumes an investment support equivalent to operational premium over the support period. It assumes that the operational premium comes from developed countries. Therefore, a discount rate of 3% is used to calculate the real cost of operational support for supporting the state. An investment equivalent to the same overall support as operational premium in the previous example decreases the green hydrogen LCOH in Southern Africa by 60%.

Investment support can reduce both financing costs and investment costs as it can reduce the liquidity requirements at the beginning of the project. The green hydrogen LCOH with investment support is 28% lower than with operational support considering the same support expenses for the funding state. This results from the asymmetry between public interest rates and the weighted average cost of capital, and injection of the whole amount of support at the beginning of the project which helps reduce both investment and financing significantly. Investment support is suggested to be more beneficial both from a hydrogen producer’s point of view due to its predictability, and as it is bifurcated from the output levels of the production facilities, which can also be translated to less exposure to production risks.

- Facilitating permitting processes

Ambiguities in permitting approval time and material availability can entail delays before the projects’ operation. Construction time of green hydrogen production facilities can vary from 1 year to 3 years. Delays in the commissioning can delay the first revenues of the production plant. These revenue delays can have an impact on the project’s Net Present Value (NPV) and LCOH. LCOH is increased by 5% with a delay of 1 year and 14% for 2 years.

Support mechanisms can impact the economic and financial viability of green hydrogen projects differently. Operational and investment support mechanisms can increase the bankability of green hydrogen projects. Nevertheless, in the current grounds where the environmental impacts of grey hydrogen are not reflected in its market value, increasing competitiveness of green hydrogen projects requires not only supply-side subsidies but also ambitious carbon taxing and other mechanisms to help create a level playing field for green hydrogen projects. Deloitte’s analysis shows that one of the main enablers of competitiveness of green hydrogen in developing economies is enabling suitable financing conditions. Reduced WACC to the similar levels as the developed economies can bring the financing costs down and render green hydrogen projects bankable in the developing economies. This stems from high capital intensiveness of green hydrogen projects. In addition, this analysis suggests that investment support can be more efficient than operational support such as IRA, thanks to their higher effect on the LCOH of green hydrogen. This can also bring a significant increase in the NPV of the projects.

Access the complete paper here