This is an extract from a recent report “POWER SHIFT: Staggering rise of renewables positions China to end new coal power before 2030” by Climate Energy Finance.

China has the world’s largest power system, and it is continuing to undergo a significant transformation – from traditional coal-reliant power system to renewable and nuclear-led power system, backed up by PHS and BESS. The IEA and CREA forecast that China will peak coal-use in 2023. CEF forecasts that China can peak then plateau in coal use over the six years to 2030, followed by a slow continued decline of 2% p.a. in coal use in absolute terms in China from 2030-2040, giving a 20% decline over the next decade. China’s electricity market is at the forefront of a transformative journey from traditional thermal power generation to robust expansion of renewable energy installations. China’s shift towards greener energy sources holds immense significance not only domestically but also in the global energy transition landscape.

By the end of CY2023, China added 302 GW of zero-emissions capacity to the national grid, taking up 84% of the total newly installed capacity of the year. Over half of the national installed capacity was zero-emissions capacity, reaching 1,529 GW. While thermal power still dominates China’s electricity generation, constituting 70% of the total output, forecasts shown in Figure below from IEA suggest a transformative trend. From 2023 onwards all of China’s electricity demand will be met by renewable energy and nuclear power thanks to the continuous strong solar PV and wind power expansion, as well as the increasing nuclear power capacity. The role of coal in China’s power system will change from being the pillar energy source to serve as a supportive role for renewables.

CEF forecasts that China can peak then plateau in coal use in the electricity sector over the six years to 2030, followed by a slow continued decline of 2% p.a. in coal use in absolute terms in China from 2030-2040, giving a 20% decline over the next decade. Any acceleration in zero emissions capacity additions beyond our current forecasts and / or sustained acceleration in energy productivity as the Chinese economy continues to shift away from secondary manufacturing and construction towards tertiary sectors would mean that China could well deliver well in advance of its ‘double carbon’ targets – peak carbon emissions by 2030 and reach carbon neutrality by 2060. In this section, CEF will deepdive into each energy source, explore its trend, restraint, and opportunities.

Coal-fired Power Plant

With the drastic increase in the buildout of renewable energy capacity, China is expected to show a decline in coal-fired power plant generation. Although in 2023, thermal power still accounted for 70% of the total power generation (down only marginally from 72% in 2019), CEF forecasts that China will peak then plateau coal-use well before 2030 as a result of massive renewable energy scale-up. Coal will progressively decline as the central pillar of China’s power generation, and continue to shift towards a more backup role in ensuring national energy security. However, CEF notes that this scenario will require a substantial shift to cease building new coal-fired power plants, so that China can deliver its ‘dual carbon’ targets and take the responsibility as the world leader in all front renewables. The IEA indicates that the coal-fired power generation will decline through 2026 despite new coal plants having been permitted or commissioned since 2022. China will keep building new coal-fired power plants as backup power generators for the purpose of energy security.

Solar

Solar power is growing rapidly in China, in both the national electricity grid and its domestic solar manufacturing and export capacities. After a record 217GW of solar installs in 2023, China installed another 37GW of solar In the first two months of 2024, 70% of net new capacity adds and growth of 80% y-o-y. Acknowledging solar is still only 3% of total Chinese electricity generation, the disruptive effect of massive new intermittent, zero emissions, low cost solar is already being increasingly felt. With solar module prices down 50% y-o-y in the last 12 months alone, and massive new technology improvements in module efficiency still to come, CEF forecasts an average 315GW p.a. of new solar installs in China over 2024-2030.

Solar power has been China’s fastest growing VRE source during the year 2023. China added 217GW of new solar power capacity into the national electricity grid last year, accounting for 60% of the total newly installed capacity during CY2023. The CEC forecasts that by the end of 2024, China’s installed solar capacity will reach 780GW.

With China’s fast solar power deployment, CEF forecasts that by the end of CY2030, China will have 2,804GW of solar capacity installed nationwide. By the end of CY2040, China will have 6,104GW of installed solar capacity. From 2024 to 2030, China will install 314GW of new solar capacity per annum, 330GW new installed solar capacity per annum from 2030 to 2040. By 2030, China’s solar power will generate 1,791TWh of electricity, 15% of the total power generation. By 2040, China will generate 4,810TWh of electricity from solar power, accounting for 30% of the total power generation.

Distributed Energy Resources (DER): Figure below reveals that China’s solar capacity expansion, particularly during 2021 and 2022, was primarily fueled by rooftop solar installations. In 2022, small-scale solar new installations reached more than 51GW. China’s newly added distributed solar in 2022 alone is more than what the US has installed in distributed solar, utility solar and onshore wind additions combined in 2022. The transition in solar installation dynamics is further complicated by China’s unique urban landscape, characterised by limited land availability, particularly in densely populated urban areas dominated by high-rise buildings and skyscrapers. China faces challenges in deploying decentralised energy resources (DERs) in urban settings. To address this, China is prioritising the expansion of transmission infrastructure to meet rising electricity demand while minimising land use conflicts and ensuring sustainable energy growth.

Land Use: With the massive scale of renewable energy build-outs, land use issues come to policymakers’ attention. A new study conducted by Tsinghua University in Beijing and at the University of California San Diego suggests that China will run out of land on the east coast to build more renewable energy plants. Two-third of usable land for utility-scale solar will be utilised by 2060 in the east coast provinces.

Technology improvement: Technology innovation in solar panels also makes building large-scale solar projects in the desert feasible. Cleaning solar panels is another logistics China needs to deal with, especially for solar panels in the desert. Canadian Solar developed BiKu bifacial panels which can produce up to 30% additional power from the back side.

Agrivoltaics: Another innovative way of reducing the limits posed by land use conflict is agrivoltaics. Agrivoltaics are emerging in China’s rural area, a combination of food farming and PV generation is helping local farmers to profit more while reducing land use conflicts.

Wind

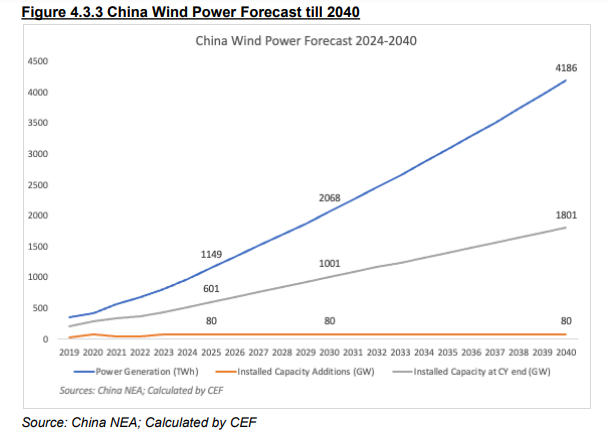

China is by far the world leader in both annual and cumulative onshore and offshore wind installations, adding a record 76GW in 2023, a 65% global share, ten times the installations in the US, #2 globally. China is also world leading in new turbine RD&D, installing in 2023 the world’s largest turbine at 18MW. This highlights the scale and momentum of China in the race to build zero emissions industries of the future. CEF forecasts 80 GW p.a. of installs out to 2040, inclusive of offshore wind, such that wind contributes 18% of total 2030 and 26% of 2040 generation, up from 9% in 2023.

The CEC forecasts that by the end of CY2024, the installed wind capacity will reach 530GW, implying CY2024 installs of 89GW, compared to the average of 50GW p.a. added over the previous 5 years. CEF forecasts that China will add an additional 80GW of wind capacity per annum from 2024 to 2040. By the end of CY2030, China will have 1,001GW of installed wind capacity nationwide; wind will generate electricity of 2,068TWh during CY2030, contributing a 12% share of total generation. By the end of CY2040, China will have installed wind capacity of 1,801GW, and electricity generated from wind power will reach 4,186TWh.

Onshore Wind: The levelized cost of electricity (LCOE) of China’s onshore wind dropped to a very competitive level of US$0.027/kWh in 2022, reducing 53% in the past 5 years, as presented by Goldwind. China’s average construction cost of onshore wind in 2022 lowered to $1,103/kW, falling 15% relative to 2018. The global average construction cost for onshore wind in 2022 was $1,274/kW.

China saw significant new policy support in 2023 for the deployment of green energy:

- January 2023 the State Council Information Office released the white paper “China’s Green Development in the New Era”, proposing to promote green and low-carbon energy development and vigorously develop non-fossil energy.

- April 2023 saw the NEA issue the “Guiding Opinions on Energy Work in 2023”, proposing to further promote structural transformation and increase the proportion of non-fossil energy in total energy consumption

- June 2023 saw the NEA release the “Blue Book on the Development of New Power System”, proposing the overall structure and key tasks of building the new power system.

- August 2023 saw the NDRC, the Ministry of Finance, and the NEA jointly issue the “Notice on Full Coverage of Renewable Energy Green Power Certificates to Promote Renewable Energy Electricity Consumption”, proposing to issue green certificates for all the electricity produced by registered renewable energy power generation projects nationwide to achieve full coverage of green certificate issuance.

- October 2023 saw the Ministry of Ecology and Environment issue the “Notice on Completing Greenhouse Gas Emission Reporting and Verification of Enterprises in Certain Key Industries from 2023 to 2025”

- November 2023 saw the NDRC issue the “Opinions on Accelerating the Establishment of Product Carbon Footprint Management System”, proposing that by 2025, about 50 key product carbon footprint accounting rules and standards will be introduced at the national level, a number of key industry carbon footprint background databases will be initially established, a national product carbon label certification system will be basically established.

Offshore Wind: The GWEC estimates that China will add approximately 12GW of offshore wind per annum from 2024 to 2025, and 15GW per annum from 2026 to 2030. The IEA estimates that China will add approximately 12GW of offshore wind per annum from 2023 to 2028 under their main case scenario. CEF forecasts that China will add 15GW of offshore wind per annum from 2024 to 2040, which means China will add a total of 255GW of offshore wind, which is entirely feasible based on the 309GW total offshore wind capacity upside proposed by SPIC. Offshore wind has a significantly higher per MW capital cost of deployment, but much larger scale, a materially higher utilisation factor, land constraints, proximity to demand centres, leveraging China’s existing ship building capacities, excess steel manufacturing capacity plus low and declining interest rates in China all support the deployment in China, as in Northern Europe.

Hydro

China has by far the largest fleet of hydroelectricity capacity, reaching 422 GW of installed capacity by February 2024, four times the capacity installed in the US, the world’s second largest hydro market. CEF expects China’s new capacity installs of hydro will slow significantly to average just 2GW p.a. over the coming decade, down from the 13GW p.a. added in the last five years, given the physical limits have nearly been reached.

China’s hydropower was hit severely by drought across the country in CY2023. China added 8GW of hydropower to the grid during CY2023, representing 2% of the newly installed capacity, a 66% y-o-y decrease. By the end of CY2023, China’s total installed hydropower capacity reached 422GW, a 1.9% y-o-y increase. During CY2023 hydropower generated electricity of 1,141TWh, a 5.1% y-o-y decrease. IEA points out that the decline in hydropower generation was a key factor in the increased use of coal-fired power generation while the electricity demand was rising in 2023

Hydropower has been the most traditional renewable energy source globally, however recent droughts in China highlighted the volatility in hydropower generation. The IEA forecasts that in 2024, VRE will generate more electricity than hydropower. In 2028, hydropower will still be the number one renewable electricity source.

CEF forecasts that China will add an additional 2.4GW of hydropower capacity per annum from 2024 to 2030, and no more hydropower addition after 2030. By the end of CY2030, China will have 438GW of installed hydropower capacity nationwide; hydropower will generate electricity of 1,436TWh during CY2030. By the end of CY2040, China will have 438GW of installed hydropower capacity, and electricity generated from hydropower will reach 1,438TWh.

Pumped Hydro: In distinct contrast to hydro for generation of electricity, closed loop PHS is surging in China, with the current 8-10GW p.a. of new additions in the last few years expected to accelerate, consistent with the national target of 120GW by 2030. Along with BESS, grid modernisation, DRM and V2G, PHS will play an increasingly important role in grid reliability and balancing as ever more VRE is added to the national system. With the massive scaling up of wind and solar power in China and elsewhere, pumped-hydro storage is a good tool for a more balanced power system. The State Grid Corporation of China operates a 3.6GW Fengning Pumped Storage Power Station. The facility has 12 reversible pump generating sets, each of them has the capacity of 300MW, and a power generation capacity from storage of 6.6TWh.

Nuclear

CEF forecasts 108GW of nuclear capacity by 2040, double the current 57GW. But even with an average utilisation rate of 85%, this would see nuclear contribute just 5% of total 2040 generation, a share flat on that seen in 2023. The China Nuclear Energy Association (CNEA) says that nuclear power generation is expected to account for 10% of the country’s total power generation by 2035, and 18% by 2060, reaching 400GW of capacity. Nuclear power will play an increasingly important role in China’s process of greening the national electricity grid. The IEA forecasts that China’s nuclear generation will reach 642-661TWh by 2030.

A Smart Grid Transmission System

The energy system transformation is being critically enabled by a smart national grid transmission system. China’s grid system has by far the highest deployment of smart metres (over 400 million), and is increasingly incorporating world leading distributed energy resources and is managing the inevitable need for flexible demand and supply to accommodate low cost but intermittent renewables. China leads the world in hybrid power developments, flexible new coal power plants, as well as BESS and PHS, and V2G is soon to be deployed nationally. All of this has been supported by some $80bn annual investment in grid capacity expansion and modernisation over the last decade. CEF expects this ongoing investment to accelerate through to 2040 as China continues electrification of everything, including transport.

Wind and solar curtailment has been an ongoing road bump for China State Grid and Southern Grid to tackle. The IEA reports that China has been investing $80bn p.a. for the last decade in building out and modernising its electricity grid transmission and distribution, individually well in excess of any other nation. China State Grid alone has a $70bn grid capex target for 2024, showing this grid modernisation and expansion continues apace. New policy developments are a feature in support of the ongoing grid modernisation investments in China.

Grid Curtailment of Renewables: Historically, China built its wind and solar farms in the northwestern region, such as Shaanxi, Gansu, and Ningxia with abundant natural renewable resources. With strong GDP growth and climbing electricity demand elsewhere in China, power generated by wind and solar from afar was curtailed due to the lack of grid connection. Wind curtailment rate peaked in 2016 reaching 50TWh. China’s massive deployment of solar and wind power has been a world-record in 2023. With 76GW of wind and 217GW of solar capacity addition in 2023 alone, representing 102% and 148% y-o-y increase respectively. Building such a significant amount of new capacity a long way from the central demand precincts in East China on top of keeping up with strong ongoing electricity demand growth in the national grid has led to challenges in higher wind and solar curtailment. China lowered its curtailment rate from 20% in 2016 to 2-3% in 2022. Another way of resolving the curtailment is to build more hybrid projects.

Grid Firming: With the rapid expansion of solar and wind power across the country, the development of grid connectivity and stability become more important than ever to ensure energy security in China. China is currently facing challenges in grid bottlenecks. Some installed renewable energy capacity is not being connected to the grid as a result of lack of grid facilities. And some renewable generated power is facing curtailment due to the limit of how much electricity can be absorbed by the grid. China’s VPPs are experiencing significant growth, driven by the imperative to address challenges posed by the integration of renewable energy sources into the grid and to advance China’s decarbonization objectives. China’s large policy-driven support for solar and wind industry has led to overcapacity and oversupply in wind and solar manufacturing, causing manufacturing glut globally and driving prices for solar and wind components down significantly.

BESS

BESS are set to play a massively scaled up role in stabilising and firming electricity grids globally as the penetration of low cost, zero emissions but intermittent renewable energy grows rapidly. China already leads the world in BESS deployments, accounting for a 50% global share in 2023. CEF expects China’s BESS investments to accelerate at far more than 30% CAGR over the coming decade. Incorporating massive VRE capacity into the Chinese national grid will remain a major engineering challenge.

Leveraging the massive economies of scale, rapid cost reductions and R&D breakthroughs underpinning China’s NEV development, BESS are being rapidly deployed across China to manage the intermittency of renewables, and the vast scale and geographic dispersion of the national electricity market. President of China Southern Power Grid in March 2024 estimated that China quadrupled its BESS capacity in 2023. Combined with accelerated inter-province grid connectivity and PHS, grid reliability will be sustained.

Wood Mackenzie forecasts global installed BESS capacity will grow at a CAGR of 30% over the coming decade, led by China with a global share of ~50%. Another solution to better coordinate the electricity grid to ensure energy security and stability is to build more energy storage systems. China’s technology innovation in BESS has been pushing the market forward. China’s current energy policy requires renewable energy plants to have a storage of 20% of the generation capacity integrated to the plants, with at least 2-4 hrs duration. This is increasingly the least cost electricity solution. Distributed energy and storage solutions are forecast to boom, including the “batterification” of tools.

Access the complete report here