This is an extract from a recent report “Inflection Point: The State of US PV Solar Manufacturing & What’s Next” by Guidehouse Insights.

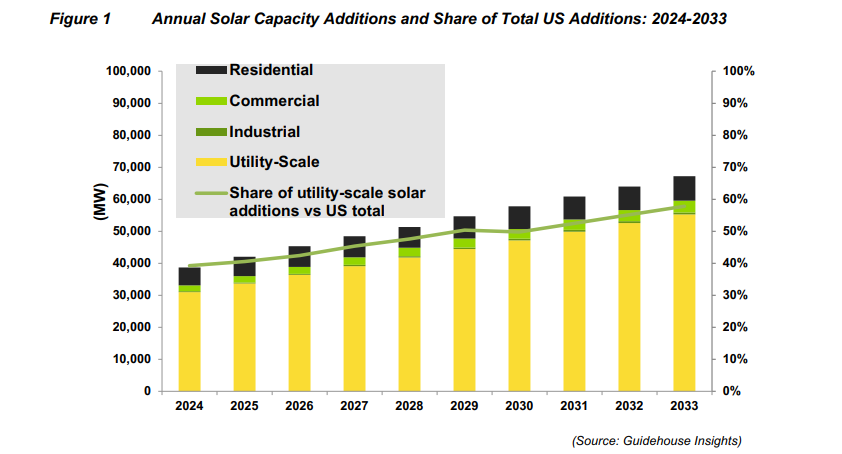

The US solar electricity market remains strong, accounting for almost half of all utility-scale generation added to the US power grid. Because US solar energy is a source of electricity with one of the lowest CAPEX in most parts of the country, demand is only expected to accelerate through 2035 and beyond as governmental policies and demand for nonpolluting energy continue to grow. Solar energy today is an affordable, accessible, and viable method for powering the energy transition in the US.

However, US-China geopolitical relations and the attendant implications for American energy security remain a core challenge for the transition to solar as a more integrated part of the US energy grid. The country is in the precarious position of being overly reliant on imported goods largely from Chinese controlled companies to meet its rapidly increasing solar demands. Over the last decade, the Chinese government has heavily subsidised the growth of its own domestic solar manufacturing market, while America’s domestic manufacturers have not received comparable levels of support.

The US currently has the makings of a strong solar manufacturing supply chain, but increased support is critical to regain solar manufacturing competitiveness. Filling these support gaps is possible, and in doing so, the US can improve its energy security and market leadership as the world increasingly looks to solar PV technology to generate low cost electricity in the face of the continuing climate crisis. Strong, consistent, and unwavering policy support for domestic solar manufacturing can lay the foundation to make the US, the nation that invented solar modules, a leader in modern solar energy manufacturing.

In the early days of solar adoption, technology providers made enormous efforts to lower the CAPEX needed to deploy solar PV systems to make them competitive with fossil fuel sources. Residential solar PV system costs dropped from nearly $9 per watt in 2010 to just over $3/W in 2018. Similarly, utility-scale solar PV system costs went from roughly $6.50/W to $1.35/W in that same period. However, in the years since, the cost decreases to deploy solar have become significantly less dramatic. Demand for solar has continued to increase, while the prices for competing energy sources, such as natural gas, as well as the soft costs associated with the deployment of solar such as transmission queues and permitting, have remained high.

Supply Chain Analysis Shows Glaring Gaps for US Ingots, Wafers, and Cells

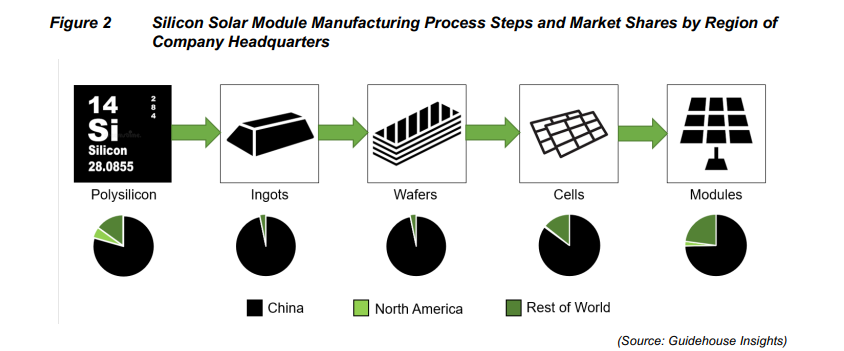

While solar energy technology was invented in the US, domestic manufacturing capacity has only achieved a fraction of what is possible. The US is highly dependent on China for much of the polysilicon PV supply chain, which includes the processing of mined quartz into high quality polysilicon, the pulling of ingots, slicing wafers from the ingots, the production of solar cells, and the final assembly into solar PV modules complete with weatherized housing. Polysilicon facilities in Michigan, Tennessee, and Washington currently form a foundation for a larger domestic supply chain, but more support is needed to grow domestic manufacturing. The IRA and the CHIPS Act were valuable first steps that will support the opening of multiple new research, development, and manufacturing facilities in the US. While these are positive steps toward a stronger solar manufacturing position, more action is needed to secure a domestic energy future that can withstand international supply chain disruptions.

The country lacks critical next-step manufacturing facilities for the various refinement and component fabrication steps in the solar cell manufacturing process. The US also lacks capacity to manufacture ingots, wafers, and cells, and therefore is entirely dependent on global suppliers for these components. This is in stark contrast to 2014, when the US had nearly a dozen facilities involved in ingot and wafer production with a capacity of around 500 MW. These manufacturing steps are the most capital intensive yet among the least incentivized through the provisions in the IRA.

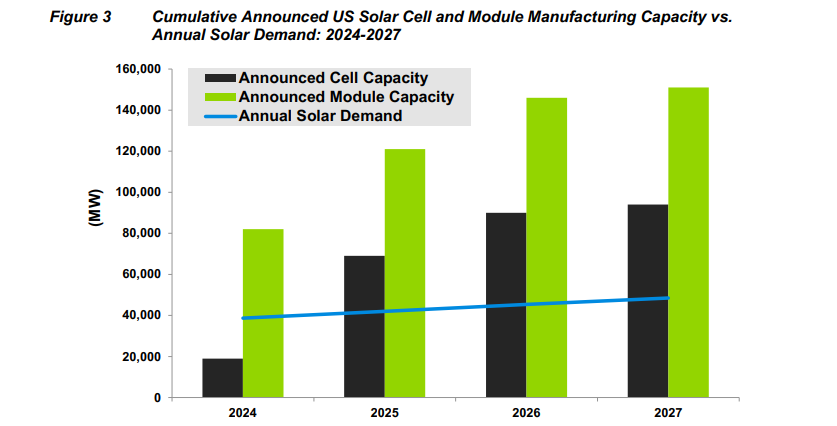

As a direct result of IRA provisions, the US is seeing a significant increase in announced cell manufacturing and module assembly capacity. If even half of this announced capacity comes online, the US could produce enough cells and modules to meet nearly 100% of its new solar demand through 2027. If no new factory capacity came online after 2027, the country could still meet more than 90% of its new solar demand in 2028, dropping slightly to roughly 70% of new demand in 2033.

Figure below shows projected solar demand and announced cell manufacturing and module assembly capacity across all types of solar PV technologies from 2024 through 2027. While this growth in the final phases of solar manufacturing capacity is a promising start, the US is still overly dependent on large amounts of imports from Chineseowned companies for upstream materials to meet rapidly accelerating demand.

China’s Dominance Disadvantages US Manufacturers and Results in Stockpiling

While the US has taken many positive steps in recent years toward bolstering its solar manufacturing capacity, several critical issues must be addressed to achieve domestic market security. In the global market, the US produces only about 5% of global polysilicon supply and final assembled solar modules. China today produces more than 90% of solar-grade polysilicon, and Chinese-owned companies control 80%-95% of global shipments across the solar supply chain.

Another major threat to building up US solar manufacturing capacity is the stockpiling of cheap imported cells and modules. The Biden administration’s decision to declare an emergency moratorium on assessing duties on solar products originating from China and routed through Southeast Asia has resulted in a major increase in the availability of cheap solar imports.

Onshoring Solar Production Will Aid Industry and End Users

With the volatility of a global solar supply chain as well as mounting geopolitical conflict between major players in the global solar industry, onshoring solar manufacturing is more critical than ever as the US looks to increase its deployments of solar energy to keep pace with growing domestic demand. Building a fully domestic solar supply chain that includes every step of the solar manufacturing process would allow the US to capture more of the workforce and economic benefits of the clean energy transition while ensuring a secure and reliable supply chain.

Breaking the reliance on foreign entities for key solar panel components would also enhance US energy independence and security. Solar PV prices are inherently volatile, even on a 6-month horizon. Increasing domestic solar manufacturing capacity will not only strengthen the country’s supply chain and insulate it from global disruptions but will also help create new, high paying, permanent jobs for skilled workers. Job creation is essential to facilitating the energy transition in the US, and it is imperative to ensure support for such efforts remains high.

Domestic Solar Manufacturing Capability Increases Energy Security and Reduces Global Supply Chain Disruptions: Increasing onshore manufacturing capabilities can help limit module price volatility and availability disruptions, most of which stem from international events. Throughout the solar panel supply chain, world events can and often do negatively affect the availability, and therefore the price, of required resources to produce panels. Impacts from COVID-19 led to a 38% decline in the US solar workforce, a 37% decline in forecast US solar installations, and a loss of approximately $3.2 billion in economic investment. Increasing US solar manufacturing capacity would also make solar components more readily available, in turn reducing US exposure to international competition for these key parts. Because of China’s relative dominance in the global solar manufacturing supply chain, Chinese manufacturers exercise a significant amount of influence over the global solar market.

Module Cost Has Limited Impact on Customer Adoption: Module cost is a common concern with onshoring solar manufacturing because goods manufactured overseas tend to come at a lower price. This concern is driven by fears that high prices for modules made in the US may lead to slower consumer adoption. However, continued module cost declines will likely have limited impact on customer adoption of solar moving forward. Potential cost reductions in other areas of solar deployment (i.e., permitting, installation/overhead, and balance-of-system operations) are likely to have a larger impact on market growth. An additional potential barrier to adoption not related to cost is a lack of qualified workers and long interconnection queues, which are leading to project delays.

Onshoring US Solar Manufacturing Will Create More Skilled Jobs: One of the largest benefits of onshoring US solar manufacturing capacity will be the creation of a large number of skilled jobs. Employment at any stage in the solar manufacturing process can offer high wages, full benefits, a steady line of work in a permanent location, and opportunities for career progression, all of which also supports the surrounding economy. The passage of the IRA has already resulted in several announcements of new domestic solar manufacturing facilities, which should lead to a significant increase in solar manufacturing job openings.

Onshoring solar manufacturing reinforces economic growth and invites qualified personnel and highly educated workers with technical backgrounds to enter the solar job market. However, manufacturing is not the only sector that would see new jobs generated by onshoring the US solar supply chain. As production ramps up, additional R&D jobs in the solar industry may also be created as alternative cell technologies and manufacturing processes are explored to keep pace with demand. These jobs can lead to advances in equipment, technology, and materials that may facilitate sustainable and rapid growth in the solar industry.

Establishing more domestic manufacturing jobs in the solar sector could also boost national support for clean energy technologies and bolster the clean energy transition. If people are employed by an industry, they may be more likely to support policies related to furthering that industry. US jobs created in the solar industry, particularly manufacturing jobs, can counter the often cited argument against transitioning to green energy that closing fossil fuel plants will eliminate jobs.

US-Made Solar Materials and Components Are Produced While Adhering to Stricter Environmental and Labor Standards: Onshoring the production of polysilicon, wafers, cells, and modules allows the US to better regulate how the components are produced from end to end. Securing domestic ingot and wafer capabilities is essential to facilitating further investment in more downstream domestic capabilities like cells and modules. Without capabilities at each step in the manufacturing process, US-based cell and module manufacturers would still be subject to Chinese-owned polysilicon and wafer suppliers. Onshoring the solar supply chain means US regulatory agencies would have more control over the material sourcing and manufacturing process of the components themselves, which can result in higher quality and more ethical and environmentally sustainable production than seen overseas, where it can be difficult or impossible to confirm that ethical practices are being observed.

For instance, after the US passed the Uyghur Forced Labor Prevention Act (UFLPA) to prevent the use of goods sourced through forced labor in China, the Forced Labor Enforcement Task Force (FLETF) was charged with developing an enforcement strategy that first established a rebuttable presumption whereby entities are preemptively barred. It is then the responsibility of the importer to produce the proper evidence to refute that presumption about its goods. The UFLPA requires the FLETF to provide annual updates to its enforcement strategy, criteria for barring entities, and the list of barred entities. Because China controls the majority of manufacturing of certain products, such as polysilicon, it is difficult for US consumers of such products to thoroughly ensure their supply chain is free of forced labor.

Public and Private Sector Collaboration Is Needed to Facilitate US Solar Manufacturing Investment and Innovation

Increasing domestic manufacturing capacity, in any field, after it has largely moved overseas is a challenge. In the solar industry, it will require extensive collaboration between the government, investors, and technology companies. The current US solar manufacturing supply chain is fragile and heavily reliant on imported materials from China and Southeast Asian countries; however, the industry’s outlook in the US is optimistic. The US has many of the building blocks in place for a strong domestic solar manufacturing supply chain but needs further investment and innovation from a variety of stakeholders to address the gaps.

Create and Enforce a Supportive Policy Environment Long-Term: Perhaps one of the largest drivers for increasing US solar manufacturing capacity is the creation and enforcement of a supportive policy environment. Policies may directly or indirectly affect the economics of domestically manufactured solar components. Among those policies with influence are tax credits tied to production volumes of solar components and incentives related to upfront CAPEX for the factories producing those components. These types of policies help offset the higher cost of manufacturing until domestic factories can scale up to become cost-effective.

Vigorous Enforcement of US Trade Laws Is Crucial in the Context of Rampant Transshipment, Cross-Border Subsidies, and Duty Evasion: For almost a century, the US has employed antidumping and countervailing duty (AD/CVD) laws as the first line of defence against unscrupulous trade practices. These laws help level the playing field for US solar manufacturers that face competition from heavily subsidized and dumped imports. AD/CVD laws have been particularly important because China has heavily subsidised its solar industry and used its trade laws to block US imports to China.

Policymakers must aggressively enforce the UFLPA: Despite the Biden administration’s concerted efforts to enforce the UFLPA, challenges with the law and China’s anti-enforcement laws have made enforcement difficult. According to CBP’s own UFLPA enforcement statistics, about $1.1 billion worth of electronics was examined for UFLPA compliance in 2023, but only $200 million worth of those goods were denied. The Biden administration and Congress should enhance UFLPA enforcement to ensure that solar polysilicon supply chains are as traceable as possible and bad actors are held accountable

Promote Workforce and Facility Development: Finding enough qualified workers is critical to the US energy transition, and ramping up domestic solar manufacturing capacity is no exception. Relevant stakeholders like unions, community colleges and trade schools, utilities, developers, policymakers, and solar technology companies should look to enhance opportunities related to education and training for clean energy manufacturing jobs. Providing incentives and resources like on-the-job training, tuition assistance, flexible schedules, and knowledge centers can help potential workers gain the required skills. Some polysilicon wafer and cell manufacturing steps also have the advantage of sharing similarities with existing manufacturing processes in other industries, meaning there could be some skill overlap.

Allow Sufficient Time to Build Out Manufacturing Infrastructure: Manufacturing facilities require time to scale up production such that they can become cost-effective. Each step in the solar manufacturing supply chain has a different threshold at which that effectiveness is achieved. This means it is essential that any policies and incentives put in place to encourage the growth of domestic solar manufacturing capacity must allow for a ramp-up period. This may mean enabling a slow phaseout of imported materials such that current and projected solar demand can be met while simultaneously increasing the manufacturing capacity at each step in the solar supply chain of domestic suppliers.

Pursue Next-Generation Technologies in the Solar Supply Chain: Diversity in supply chains is essential to ensure industries can withstand disruptions and mitigate negative impacts stemming from changes to the status quo. This white paper is focused on outlining the benefits of onshoring more of the crystalline silicon solar supply chain. Within this supply chain are numerous next generation technologies that could be investigated to help introduce technological diversity. New technologies could include different types of ingots and wafers, wafering techniques (such as kerfless wafering), or cell structures. The future of US solar technologies will also likely incorporate both CSPV products as well as thin-film products.

Access the complete report here