Renewables overtook fossil fuels to become the EU’s main source of electricity for the first time in 2020. This report compiles and analyses the full-year 2020 electricity generation of every EU country, tracking Europe’s electricity transition. This is the fifth year in a row that Ember (formally as Sandbag) has done this analysis in conjunction with Agora Energiewende. Renewables rose to generate 38% of Europe’s electricity in 2020 (compared to 34.6% in 2019), for the first time, overtaking fossil-fired generation, which fell to 37%.

This is an important milestone in Europe’s clean energy transition. At a country level, Germany and Spain (and separately the UK) also achieved this milestone for the first time. The transition from coal to clean is, however, still too slow for reaching 55% greenhouse gas reductions by 2030 and climate neutrality by 2050. While Covid 19 had an impact in all countries, its impact on the overall trend from fossil fuels to renewables was quite limited. The rise in renewables was reassuringly robust despite the pandemic, and the fall in fossil-fired electricity could have been even more dramatic, had it not been for such a bounce-back in electricity demand and the worst year on record for nuclear generation.

1. Rising Renewables

Renewables are now the EU’s largest source of electricity

Wind and solar have powered Europe’s renewables rise. Wind and solar generated a fifth of Europe’s electricity in 2020. Wind supplied 14% of Europe’s electricity, up from 9% in 2015, and solar supplied 5%, up from 3% in 2015. Bioenergy* growth slowed throughout the last decade and has stalled since 2018. New hydro capacity is near-zero, the changes in hydro generation are driven only by precipitation changes.

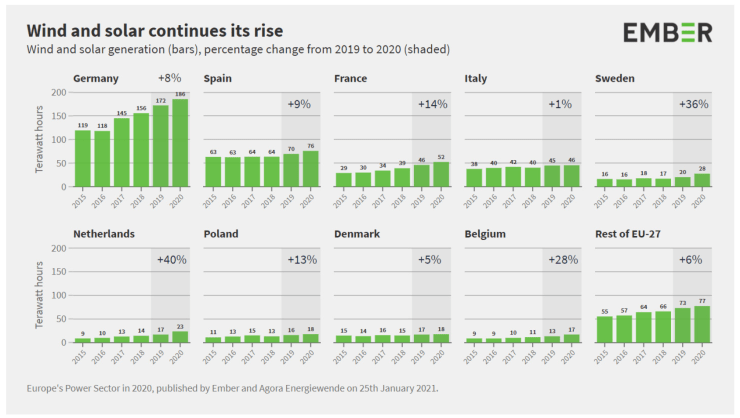

Wind and solar generation grew by 10% in the EU-27 in 2020. Netherlands saw the largest rise in wind and solar generation, as it catches up after years of slow deployment, bringing its wind and solar in line with the European average (19% of electricity production compared to 20% for the EU-27). In France wind and solar alone overtook fossils for the first time ever, marking the next green milestone, which is already met by Denmark and Sweden. The biggest increases were in the Netherlands (40%), Sweden (36%), and Belgium (28%). Many of the smaller countries not on the graphic continued to see near-zero growth in wind and solar: Austria, Portugal, Czech Republic, Italy, Romania, and Slovakia.

Leaders in wind and solar show what is possible if there is sustained political will, while some countries continue to lag behind despite excellent solar and wind conditions. Denmark generated 62% of its electricity from wind and solar in 2020, which was almost twice the next country of Ireland. Germany was third, and then Spain overtook Portugal into fourth place. Seven countries – some with excellent conditions for solar and wind – have barely seen any growth since 2015 – Portugal, Romania, Austria, Italy, Czechia, Slovakia, and Bulgaria.

Wind and solar generation growth must nearly triple to reach Europe’s 2030 green deal targets. Wind and solar increased by 51 terawatt-hours in 2020, and whilst it wasn’t a record, it was well above the 38 TWh/year average last decade. But annual additions will need to nearly triple to around 100 TWh/year to reach Europe’s 2030 target of 55% cuts to GHG emissions. That means well over 100 TWh added annually by 2030, as growth picks up through the decade. Currently, national energy and climate plans add up to only about 72 TWh/year, according to Ember’s “Vision or Division?” report, so countries still need to step up their 2030 national commitments.

Wind and solar installations were surprisingly robust in 2020 despite Covid-19, and 2021 might see record new wind and solar installations. The IEA estimates there will be 18% less wind capacity installed in the European Union in 2020 than in 2019, but that it will sharply increase in 2021 due to new growth in France, Poland and Denmark. Europe’s solar picture is brighter still: the IEA estimates that solar installed in the European Union will increase by 16% in 2020 compared to 2019 due mostly to utility-scale deployment from auctions in Germany, France and Poland, and then dramatically increase from 2021 as many countries begin to step up deployment.

Europe’s electricity demand was down 4% in 2020; although it was down 13% in April at the height of the lockdown, it then recovered to pre-Covid levels by the start of winter. The deepest reductions in April were in Italy (-21%), France (-19%) then Spain (-17%). However, all three countries recorded higher year-on-year demand in December, indicating a bounceback to normal demand levels from 2021. Against this backdrop of dramatic demand shifts, it’s not clear whether underlying electricity demand increased as electrification steps up with more electric cars, heat pumps, and electrolysers in 2020. What is clear is that this will be a driver in the future, further underscoring the need for more rapid deployment of new wind and solar.

2. Falling Fossils

Coal fell by 20%, but gas barely fell despite Covid-19

Coal generation fell 20% in 2020 and is now half that of 2015. Coal generation – hard coal and lignite – fell to 365 terawatt-hours in 2020, a fall of 48% since 2015. That is a remarkable achievement and is equivalent to around 320 million tonnes less CO2 per year, which is about 7% of Europe’s GHG emissions in 2020. Lignite generation fell 18% in 2020, its biggest fall since at least 2000; but once again this was less of a fall than hard coal generation, which is now substantially below lignite generation. Coal supplied just 13% of Europe’s electricity in 2020. Coal would need to fall to near-zero by 2030 to reach the EU’s 55% GHG emissions target, according to the European Commission’s impact assessment.

Europe saw coal fall in almost every country. Netherlands, Greece, and Spain continue to power towards phasing out coal completely, helped by good growth in wind and solar. Germany – Europe’s largest coal generator – saw its coal generation fall by 22% in 2020, slightly faster than Europe’s average of 20%. Germany even fell so much that from February to July its monthly coal generation was below that of Poland, briefly making Poland Europe’s #1 coal generator for the first time ever, as Poland’s falls in coal lag behind the rest of Europe.

Only half of coal’s fall was due to new wind and solar. Since 2015, although coal generation halved, (-340 TWh), only half of that was replaced by wind and solar (176 TWh). Increasing gas generation, and the fall in electricity demand due to Covid-19, also sped up coal’s fall. In 2020 itself, coal generation fell by 90 TWh, compared to a 51 TWh rise in wind and solar.

Nuclear generation fell a record 10% in 2020, as French and Belgian problems combined with permanent closures in Sweden and Germany. This was the biggest fall since at least 1990, and possibly ever; it’s even bigger than 2011when Germany closed nuclear plants following Fukushima. France’s nuclear generation fell by 44TWh (11%) as EDF suffered big outages. Sweden fell by 17TWh in part because of the closure of Ringhals 1 in December 2019. Germany fell by 11TWh due to the closure of Phillipsburg in December 2019. Belgium fell by 9TWh (20%) as problems persisted with its nuclear fleet. Nuclear generation will continue to fall as countries step up to phase-out nuclear: 2022for Germany, 2025 for Belgium, 2030 for Spain, and a reduction in France by 2035 to half of its electricity mix. This illustrates once more the immediate need to increase the speed of adding wind and solar capacities.

Gas generation only fell 4% in 2020, despite the electricity demand drop from the pandemic. Most of the fall in fossil fuels was on coal rather than gas in 2020 because a robust carbon price and low gas prices meant gas generation was the cheapest form of fossil generation, even undercutting lignite for the first time in some months. Fossil gas still supplied 20% of Europe’s electricity in 2020, and although gas fell in 2020, it is still 14% higher than in 2015. Greece, the Netherlands and Poland saw gas generation rise in 2020. So although wind and solar is replacing coal, no country has yet seen wind and solar starting to significantly replace gas generation. And indeed, Greece and the Netherlands have still seen rising gas generation.

Besides Poland, the countries with the largest share of fossil generation were Netherlands, Greece, Ireland, and Italy. Although coal is being phased out in Netherlands, Greece, Ireland, and Italy, their continued reliance on gas generation means they are still a very long way from fossil free electricity. Poland and the Czech Republic are the only two countries with more than four times the amount of fossil generation as renewables generation. Austria has the highest renewables share, but even there still has a lot of gas to phase out.

Coal’s fall means Europe’s electricity is 29% cleaner than in 2015. Carbon intensity has fallen from 317 grams of CO2 per kilowatt-hour in 2015 to 226 grams in 2020, falling by 10% in 2020 alone. Although coal generation has almost halved in that time, 43% of the coal decline has been offset by increased gas generation, slowing the reduction in carbon intensity. Although Germany is leading the way on renewables, its electricity still remains much dirtier than the EU average due to a relatively high share of coal. For the first time, Poland’s electricity is now the dirtiest in Europe, overtaking Estonia’s carbon intensity as Estonia reduced its carbon-intensive oil shale generation.

3. Data Methodology

For 2000 to 2018, the data is from EUROSTAT (nrg_bal_peh). 2019 and 2020 data is our ‘best view’ of what the Eurostat data will be when it is published. We do this by estimating the year-on-year changes for each year and adding them onto the 2018 Eurostat figures. To estimate these changes, we rely mainly on Ember’s monthly curated data for Europe from ENTSO-E data and cross-check these changes against any available monthly data from Eurostat, and data from national TSOs.

For Germany we use AG-Energiebilanzen for all years. Note: all data used is “gross” not “net”. As always, Entso-E data is far from perfect, so the process of estimating yearly changes is an art of piecing together multiple data sources. Notable issues with Entso-E are the classification of fossil generation in NL and IT, and poor coverage of small gas and bioenergy plants across most countries. Here are the changes seen applied to 2020 from 2019:

The article has been sourced from Ember Climate and can be accessed by clicking here