This is an extract from a recent report “Renewable Energy Manufacturing Opportunities for Southeast Asia” prepared by the Asian Development Bank, Bloomberg Philanthropies, ClimateWorks Foundation and Sustainable Energy for All.

Within Southeast Asia’s $160 billion to $200 billion sustainability revenue pools in 2030, 55 per cent – 60 per cent is driven by low-carbon mobility and clean power, representing significant opportunities for manufacturers of inputs into these sectors. The region has made headway with capturing this opportunity. In low-carbon mobility, it has seen success in attracting international and local players to set up facilities for electric two-wheeler vehicles (E2W) assembly. In clean power, the region is already a global exporter of solar photovoltaic (PV) cells and modules.

Leveraging its natural advantages, Southeast Asia could aspire to further scale its renewables manufacturing capacity and to be a key contributor to global decarbonization.

Solar PV manufacturing trends

The solar PV module manufacturing value chain comprises four main steps: polysilicon production, wafer production, cell manufacturing, and module assembly. Southeast Asia is a solar PV manufacturing hub with 2 per cent – 3 per cent of the world’s polysilicon and wafer capacity and 9 per cent–10 per cent of the world’s cells and modules capacity. Production is concentrated in four countries: Cambodia, the Lao People’s Democratic Republic (Lao PDR), Thailand, and Viet Nam. According to manufacturers’ present in Southeast Asia today, most manufacturing capacity in the region was established by manufacturers from the People’s Republic of China.

Southeast Asia is largely an exporter of solar PV products today. Its nameplate capacity of 70 GW dwarfs regional demand of ~3 GW p.a. There are three broad archetypes of producer countries in the region:

• Established global and domestic suppliers: Viet Nam, Malaysia and Thailand have large production capacities, and supply both domestic demand and a significant share of global demand.

• Export-focused markets: A key regional example is Cambodia, which has approximately 7 GW of solar PV module production capacity, of which nearly all production is exported to the United States (US) market. Domestic solar PV additions in 2020–2022 have been <100 MW per annum, and partly supplied by imported panels.

• Domestic-led markets: A key regional example is Indonesia, which has a sizable number of small-scale module assembly companies (>10 manufacturers of 30–200 MW capacity each) serving local demand to fulfil national targets for local products.

According to the International Energy Agency (IEA), in 2017–2021, Southeast Asian manufacturers supplied one-third of global PV module exports, directed mostly to the US and the European Union (EU). Demand for imports in Southeast Asia’s dominant export market, the US, is expected to shrink as it makes efforts to localise its supply chain through the Inflation Reduction Act (IRA) and other supply incentives. Europe and Southeast Asia are likely the most attractive demand markets to fill this gap, while the ability of regional players to compete in other export markets will depend on attractiveness with regard to key buying factors, e.g., price.

In export markets, cost competitiveness will be critical. The market for solar PV modules is relatively commoditized, and price is a key buying factor for solar developers. Cost differences between producers are driven by three key factors:

• economies of scale driven by stronger buying power and lower fixed costs

• lower material costs driven by integrated value chains and the presence of robust local supply chains for production inputs

• lower material and non-material costs driven by lower yield and productivity.

Battery manufacturing trends

The battery value chain comprises six main steps: mining, refining, precursor/cathode manufacturing, cell manufacturing, battery pack manufacturing, and battery recycling. Southeast Asia has significant potential to establish an end-to-end battery value chain, given its rich critical mineral resources and strong interest from global industry players to establish a domestic manufacturing footprint. Several downstream players, including local and global cathode and cell manufacturers, have expressed interest in establishing production facilities in the region.

There are currently two prominent battery technologies in the market: Nickel Manganese Cobalt (NMC) and Lithium Iron Phosphate (LFP). Southeast Asia is naturally advantaged to develop an NMC technology-focused battery ecosystem given the region’s vast reserves of nickel, which is the main raw material for NMC batteries.

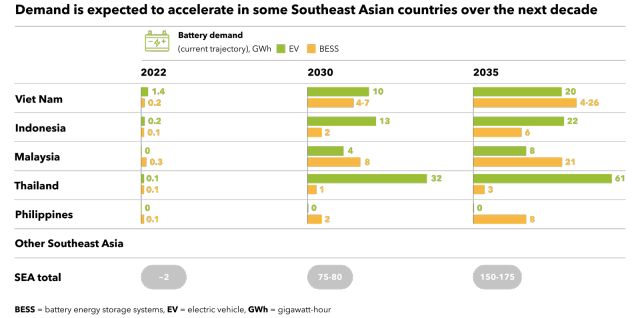

Global and Southeast Asia battery demand for battery manufacturing output from Southeast Asia is expected to be led by exports to other regions (e.g., US, Europe), despite growing regional demand. Based on the current trajectory of demand, global demand for batteries is projected to increase by approximately 25% per year to 4.5 TWh by 2030. NMC technology currently dominates more than half of total global battery demand and is expected to grow at approximately 20 per cent per year. It is expected that Southeast Asia’s demand will grow at an annual rate of over 40 per cent until 2030, reaching approximately 75-80 GWh. This demand is expected to double over the next 5 years to 150-175 GWh in 2035.

To foster growth in the battery industry in Southeast Asia, it is particularly important to target global export markets given the domestic market is growing from a smaller base. The cost competitiveness of battery manufacturers is mainly driven by four factors:

• Vertical integration and access to low-cost raw materials: Raw materials account for approximately 40 per cent of total cell production cost, leading major cell manufacturers (e.g., CATL, Panasonic, and LG Chem) to pursue integration upstream (e.g., into mining and refining) to secure access to these materials.

• Scale of production: Manufacturing at sub-scale volumes (i.e., below 10 GWh) can be less competitive due to the high labor and energy costs involved. Larger production scale significantly improves cost competitiveness by around 20%.

• Production yield: During the initial few years of operation, battery manufacturers typically experience a low yield of approximately 20%–30%. It is critical to accelerate the learning curve to attain stable production with yields of over 90% within 4 years or less, in line with leading benchmark manufacturers (e.g., in the PRC).

• Proximity to or bulk contracts with equipment and technology/electronics suppliers: Being located close to or having bulk contracts with equipment and technology/electronics suppliers can result in cost savings on both capital expenditures and raw materials used in battery cell production.

Outlook

Scaling solar PV and battery manufacturing has the potential to create significant economic and social value for the region. Investment in a manufacturing industry adds to its gross domestic product (GDP) and creates jobs during both its construction phase (i.e., facility development and expansion) and operation phase. Such impacts are cascading: through direct impact from the construction, equipment purchase, and operations; indirect impact via supply chains, with higher potential impact the more localized the supply chain is; and induced impact, with increased spending driven by income changes of employees in the value chain.

The complete report can be accessed here